CSRD Compliance – It Is Time to Act Now!

AUTHOR: JENNIFER LOUGHRIDGE

PRINCIPAL CONSULTANT

Jennifer is a Senior Executive Finance professional with 22+ years of global experience. She specialises in Finance Transformation, ESG and Continuous Improvement, with particular expertise in Strategy, Performance Management, Business Partnering, Commercial Decision-Making, Corporate Governance and Valuation.

Many organisations with a presence in the EU need to comply with the CSRD (Corporate Sustainability Reporting Directive) regulatory framework. This significant reporting and disclosure development requires the attention of the CFO, and many organisations are still unprepared. Proactive planning has never been more critical.

What is the timeline for compliance? The clock is ticking, and it’s crucial to act now.

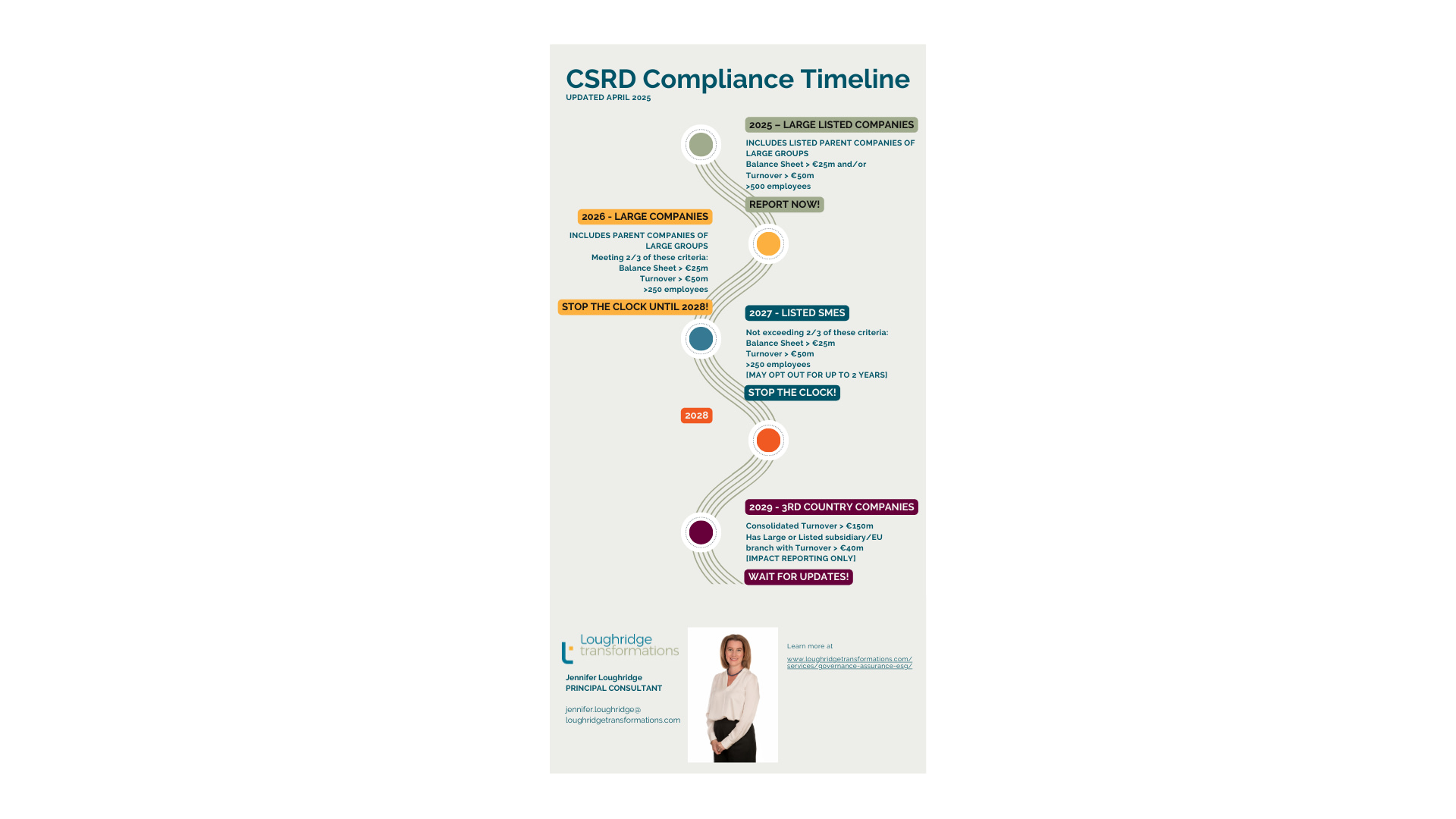

EU-listed companies that meet the turnover or balance sheet criteria and have over 500 employees must report the data points and disclosures in 2025 as part of their annual report. Many have already met this requirement.

Other EU companies meeting the above criteria (except for an employee criterion of 250) were initially scheduled to report in 2026. However, in April 2025, a “stop-the-clock” vote in the EU effectively postponed the reporting until 2028 – unless local Member State legislation requires otherwise. This delay, coupled with the ongoing review of the criteria and the potential increase of the employee criterion to 1000, adds to the uncertainty. The timing and process for these changes remain unclear.

SMEs, also known as Wave 3 entities, also benefit from the “stop-the-clock” delay.

Non-EU parent companies must begin data collection for reporting in 2029.

While the CSRD compliance deadlines for 2025 reporters will be delayed by two years from the initial proposals with the “stop-the-clock” measures, it’s crucial to note that the schedule remains tight. Until transposition, existing legislation will apply, and monitoring developments per Member State will be critical.

For organisations with more than 1000 employees, making a ‘no-regret’ plan is not just advised; it’s crucial. Even for those companies with fewer employees, reviewing the value chain and determining what will likely be important for their customers is a proactive step towards preparedness.

What sort of assurance do auditors have to provide?

The CSRD requires that the quality of sustainability information be at the same level as financial information. This means the external auditor must provide assurance on financial and non-financial information.

In the first instance, this can be provided on a limited assurance basis. As we move towards 2030, the requirement will be that the audit be performed on a reasonable assurance basis, although this remains a discussion point in the proposed simplification.

Feedback from 2024 reporters is that limited assurance went deeper than they may have anticipated, as in the first year of reporting, there is no comparative data set or, of course, previous audit.

What challenge does this present to most companies?

Under the CSRD, companies face the daunting task of publishing substantial new and highly specific information. Failing to meet these requirements could lead to severe repercussions, including reduced access to financing or an impacted market position. These risks make it clear that many companies must significantly enhance their administrative organisation and internal control framework. The days of managing sustainability reports with a simple spreadsheet are numbered, and the stakes are high.

The data requirements are qualitative and quantitative, look forwards and backwards, describe the short-, medium- and long-term, and cover the entire value chain.

The value chain requirement will likely be a hurdle in CSRD compliance for many companies. Data and technology issues relevant to meeting CSRD compliance include non-financial data collection, auditability and alignment to financial data. Furthermore, the credibility and transparency of the data and the surrounding governance can be challenging.

Is your organisation compliance-ready?

Is your organisation poised to deliver CSRD compliance?

Moreover, do you have the necessary resources, time, and expertise to achieve compliance, let alone derive value from these changes?

Would you like to learn more about what it means for your organisation and how to complete the needed actions, especially given the uncertainty created by the recent “stop-the-clock” measures and the proposal to simplify the standards?

At Loughridge Transformations, we understand you don’t want to invest time and effort in meeting compliance requirements that may never be needed…

But also, you can likely not afford to wait before making a start.

That’s why we offer a cost-effective Diagnostic and Scoping Package. This package minimises the regret work and ensures you get usable, value-accretive outcomes, whatever happens with the regulations.

Investing in a proactive compliance strategy is vital in a time of uncertainty with potential legislative shifts. Our approach ensures that you are not left scrambling when deadlines hit, allowing you to focus on delivering value to your customers while confidently meeting regulatory requirements.

Don’t let your organisation fall behind, so why not set up a complimentary ESG briefing with Loughridge Transformations‘ Principal Consultant?

This briefing will help you understand your organisation’s specific ESG challenges and how our expertise can help you achieve compliance while adding valuable outcomes.

Arrange an ESG Briefing

CSRD Compliance? What Comes Next?

At Loughridge Transformations, we possess the governance and assurance expertise to assess and recommend improvement actions and deliver robust implementation. We work in collaboration with external auditors when it is needed. Our comprehensive skillset, including governance and audit, process and control design, and project and change management, ensures sustainable improvements and ESG regulatory compliance.

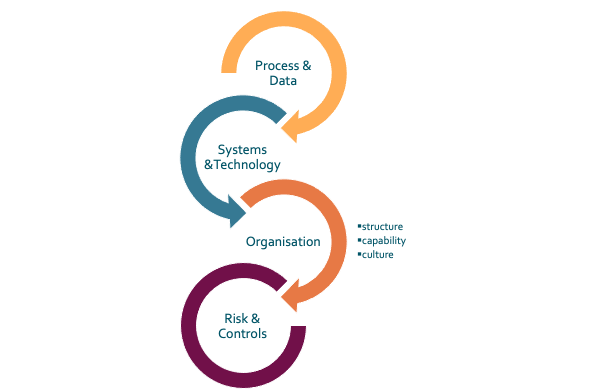

Furthermore, our design and deployment approach includes the necessary changes to the ERP, AI-enabled tools and upgrades across the Planning, Appraisal and Reporting Landscape using our Elements of Transformation model:

Our consultants have years of experience working across locations and time zones. They are also experts in delivering all services remotely or onsite in SOx (SEC), EU, UK and other regulatory environments.

We welcome any discussion on the above and more, so please get in touch!

Alternatively, take a look at our most popular blog posts:

Or are you looking for something else? Here’s what we have been blogging about recently:

Agile Analytics Associates Automation Behaviours Building Trust Business-Partnering CFO Remit Change Management Coaching Collaboration Continuous Improvement Control Design Control Framework Corporate Governance Data Deployment Digital ERP ESG Finance Function Finance Transformation Implementation Migration Off-Shoring Organisation Organisation Design Process Process Design Process Improvement Process Performance Productivity Project Management Readiness Regulatory Compliance Risk & Controls Skills sponsorship Standard Organisational Model Strategy Systems Systems Design Technology Transformation Virtual Working