ESG Compliance, Governance & Assurance

What gets measured, gets managed.

Peter Drucker

Does your organisation operate in the EU as a subsidiary or parent entity?

Then, there’s a good chance your organisation will likely have to comply with the CSRD (Corporate Sustainability Reporting Directive) regulatory framework.

Are you aware of the end-to-end scope of reporting requirements that will ultimately sit under Finance?

European Union

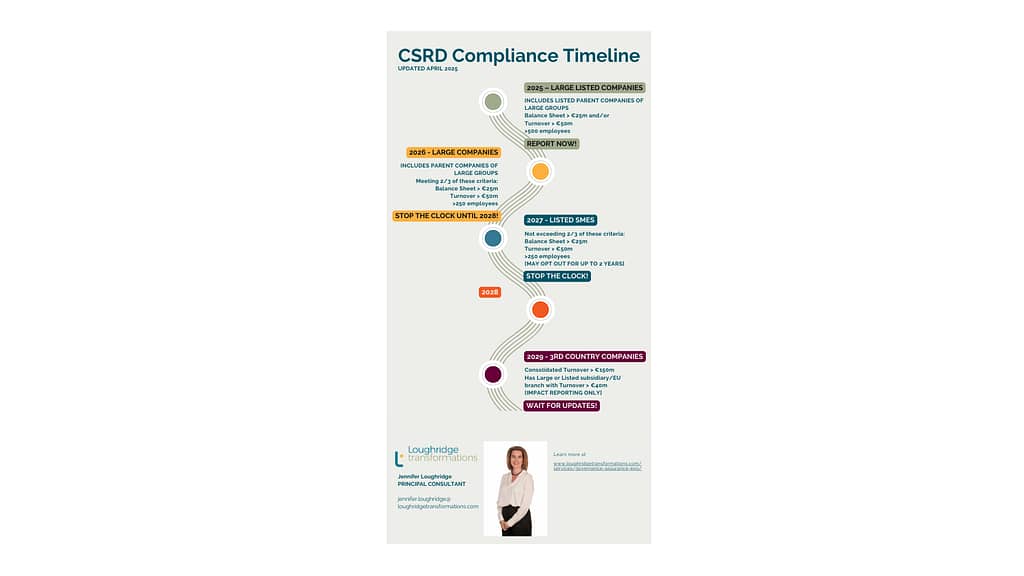

Around 42,500 companies are anticipated to be impacted. However, this may be reduced if the EU omnibus updates are approved and transposed to local legislation.

Wave 1

EU-listed companies that meet the turnover or balance sheet criteria and have over 500 employees must report the data points and disclosures in 2025 as part of their annual report. Many have already met this requirement.

Wave 2 & 3

Other EU companies meeting the above criteria (except for an employee criterion of 250) were initially scheduled to report in 2026. However, in April 2025, a “stop-the-clock” vote in the EU effectively postponed the reporting until 2028. Unless local Member State legislation requires otherwise. This delay, coupled with the ongoing review of the criteria and the potential increase of the employee criterion to 1000, adds to the uncertainty. The timing and process for these changes remain unclear.

SMEs, also known as Wave 3 entities, also benefit from the “stop-the-clock” delay.

Non-EU parent companies must begin data collection for reporting in 2029.

For organisations with more than 1000 employees, making a ‘no-regret’ plan is not just advised; it’s crucial. Even for those companies with fewer employees, reviewing the value chain and determining what will likely be important for their customers is a proactive step towards preparedness.

Depending on a specific (and subject to disclosure) materiality assessment, companies have to disclose information on the following:

- Climate Change

- Pollution

- Water & Marine Resources

- Biodiversity & Eco-Systems

- Resource Use & Circular Economy

- Own Workforce

- Workers in the Value Chain

- Affected Communities

- Consumers & End-Users

- Business Conduct

Overall, 96 European Sustainability Reporting Standards with disclosure and reporting requirements are being introduced. The audit requirements will initially be on a limited assurance basis.

Outside of the EU, other regulations are in place

IFRS

The ISSB issued the S1 and S2 disclosures in 2023. They cover climate-related processes and controls, risks and opportunities, and metrics and targets to monitor performance.

Many countries have adopted local standards based on the ISSB standards. This includes Australia, Brazil, Canada, China, Hong Kong, Japan, Malaysia, Singapore, Switzerland, Türkiye, and the UK. Others are in the process of reviewing or have made commitments to adopt the standards in the future.

UK

The Financial Reporting Council (FRC) has removed references to ESG in a new version of the UK Corporate Governance Code. The new code comes into force in 2025. However, Provision 29’s requirements around the control framework could impact the operational processes in ESG.

Furthermore, given that any material EU subsidiaries must meet CSRD requirements, many UK-listed companies may still choose to follow those standards.

Is your company ready to meet these regulatory requirements?

Do you have the resources, time, and expertise available?

Would you like to learn more about what it means for your organisation and what ESG readiness steps you should take now?

Then, why not set up a complimentary briefing with Loughridge Transformations’ Principal Consultant?

Arrange an ESG Briefing

Governance & Assurance

We use our in-house governance and assurance model, inspired by COSO, when reviewing any organisation’s control framework. It includes all or any of the pillars—business objectives, financial and climate change reporting, and compliance.

We excel in delivering solutions for our clients, whether at the client site or virtually, individually, or in teams. Working across multiple geographies, cultures, and time zones is second nature to the experienced consultants at Loughridge Transformations. They are experts in delivering all services in SOx (SEC), EU, UK, and other regulatory environments.

LT partnered with our team from early design through implementation on a project to achieve global a…Read More

Kari Ventura

LT partnered with our team from early design through implementation on a project to achieve global alignment on Finance’s future “Ways of Working.”

Jennifer and the team did a terrific job facilitating virtual and in-person workshops.

Their expertise and experience in corporate finance added incredible value to the project.

Kari Ventura

LT provided us with strong project management skills and helped us communicate and integrate the …Read More

Roddy Mackinnon

LT provided us with strong project management skills and helped us communicate and integrate the changes with a large number of people within our Finance teams. Jennifer ensured that we captured and documented the actions needed for success, even looking forward beyond the implementation date, to ensure that we remained on track, with clear visibility of progress, ensuring that the business retained ownership and accountability.

Roddy Mackinnon

I recommend the team for their expertise in applying Lean Six Sigma methodology to optimise processe…Read More

Paul Suller

I recommend the team for their expertise in applying Lean Six Sigma methodology to optimise processes, propose IT solutions and consider wider change management.

Paul Suller

Jennifer scaled the LT approach to meet our needs, demonstrating a highly flexible manner of bringin…Read More

Nick Harrison

Jennifer scaled the LT approach to meet our needs, demonstrating a highly flexible manner of bringing insights and expertise.

Nick Harrison

Our recent blogs may give some more insight into Loughridge Transformations‘ approach:

-

Aligning Financial and Sustainability Data & Reporting – Webinar Recording

Were you unable to join us live for the webinar? Or would you like to review some parts in more detail?

-

CSRD Assurance – What Finance Leaders Need to Know Now

Learn more about the CSRD Assurance learnings from 2024 reporters and what this means for your organisation and external reporting.

-

CSRD Compliance – It Is Time to Act Now!

Learn more about the CSRD compliance timeline your organisation must follow and the challenges to be faced.

-

Four Critical ESG Challenges to Think About Now!

Learn more about what these ESG challenges mean for your organisation and what readiness steps you should take to meet mandatory deadlines.

-

Getting The Most From The 2024 UK Corporate Governance Reforms

UK corporate governance reform is imminent. Find out how to leverage that to improve your organisation’s control effectiveness.

-

Powering The Net-Zero Future: Why Finance Leadership Matters Now More Than Ever

Discover how Finance leadership is driving the global shift to net-zero by 2050. Learn why Finance holds the key.