Finance Functional Fit: The Most Critical Scope Definition You Need

AUTHOR: JENNIFER LOUGHRIDGE

PRINCIPAL CONSULTANT

Jennifer is a Senior Executive Finance professional with 22+ years of global experience. She specialises in Finance Transformation, ESG and Continuous Improvement, with particular expertise in Strategy, Performance Management, Business Partnering, Commercial Decision-Making, Corporate Governance and Valuation.

In the first step of this nine-part series, we examined how to supercharge Finance Transformation. We discussed the importance of strategy, what makes it an essential step, and the strategic requirements for Finance Transformation.

-

Strategy: How to Supercharge Finance Transformation

The Loughridge Transformations approach to strategy.

This post will focus on the second of the nine steps: determining your Finance Functional Fit. First, we will review the organisation’s strategic positioning. Then, we will use a Loughridge Transformations model to determine the strategic fit of the Finance Function.

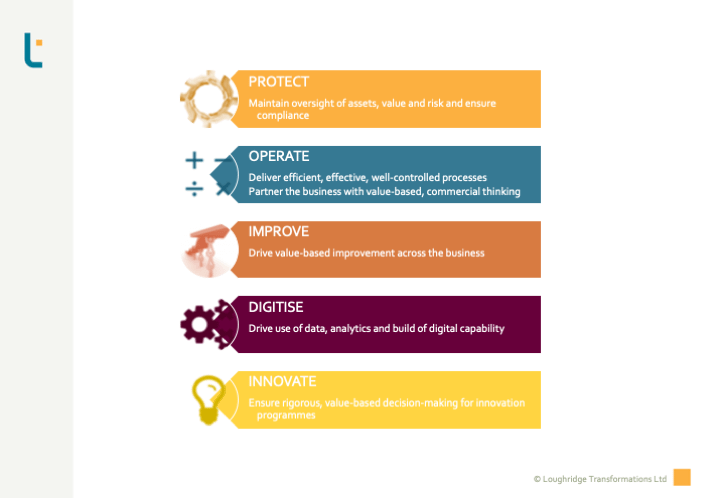

Introducing the Five-Part Finance Functional Fit Model

Now, let’s delve into the practical application of the Loughridge Transformations Finance Transformation method to determine the strategic fit of the Finance Function.

At this point, you should know where your organisation stands regarding scope and competitive advantage. If not, you need to revisit the first step!

Critical to any Finance Transformation is determining the remit of the Finance Function – confirming the scope and boundaries. Whether or not your organisation has an Enterprise Process Model, this scoping is essential in establishing the programme and defining the objectives. Subsequent steps depend on this level of clarity.

Here’s where Loughridge Transformations uses one of their expert models. Our Five-Part Functional Fit model is iterative and flexible and delivers everything you need for a successful programme where your finance objectives are aligned with your overall business strategy.

As with many parts of the Loughridge Transformations method, we offer clients the option of a standalone facilitated workshop to deliver this step in Finance Transformation.

The Finance Functional Fit model is not a rigid structure. It is designed to be iterative, with each part building on the preceding one, ensuring adaptability and flexibility.

1: Protect

This part is often referred to as a table stake or the foundation. This critical role oversees the organisation’s assets, value and risk while ensuring compliance. Examples of activities in this part include Corporate Governance, Assurance and Risk Management.

It is the foundation of the model. Consequently, these activities are rarely optional. Therefore, in almost any organisation, the finance function will have these activities as part of their remit.

2: Operate

The “Traditional” Remit

Building on that foundation, next comes what we call Operate. Delivering efficient, effective and well-controlled processes builds upon the Protect foundation. It ensures it can be done cost-effectively and reliably, using data and technology well. It is a relatively large block of activity and includes most of what we traditionally regard as the remit of the Finance function.

Business Partnering

Next to that, however, also comes partnering with the business in value-based, commercial thinking. Different organisations are in various stages of operating this way. However, it is now, more or less, the conventional wisdom that this is a core activity of the Finance function. Loughridge Transformations has expertise in supporting finance organisations in developing the structures, skills, and behaviours necessary to excel in business partnering.

Define Boundaries & Responsibilities

It is also a reasonable time to consider the scope of operations for the Finance function. What are the CFO’s accountabilities? Different organisations define the boundaries between functions differently. They make different choices on who is accountable for what. However, that is not always easy if no enterprise process model exists. At a minimum, it is essential to be transparent about processes with clear accountability and those where there may be less. This clarity helps with prioritisation further along in Finance Transformation.

Best practices exist here regarding structure and, of course, efficiency and effectiveness. So, whether you are interested in learning what other organisations do, what forward-looking research and thinking indicates, or undertaking a more formal benchmarking exercise, the Loughridge Transformations consultants can support you.

3: Improve

Following Protect and Operate, the next block of activity is Improve. These activities comprise value-based improvements, such as leading continuous improvement or championing commercial developments. They connect firmly with the business partnering activities within Operate. It is also worth reviewing the boundaries between functions in this block, as the boundary lines can often be somewhat muddy.

4: Digitise

This part is a more recent addition, with the advent of digitalisation. It includes driving data analytics and building the requisite digital capability for automation and further. Digital Transformation for the entire organisation may be done through the Finance function. As the role of Finance evolves, so do the activities for which it is accountable. Therefore, it is essential to be clear about this block of activities. Undoubtedly, the skills and organisational structures may differ from those of traditional Finance.

Moreover, digitalisation is not about replacing complete roles with machines. Studies reveal that only a percentage of activity within any role is subject to automation for the vast majority. There are also brand new roles with digital activities. These require different and developing skills and ways of working from Finance professionals.

5: Innovate

Finance is involved with value-based decision-making across the board and no less so in innovation. Consequently, the degree of innovation in the organisation will drive the activities for which Finance will be accountable.

Based on the organisation’s scope and competitive advantage, a reasonably high-level definition of where you want your Finance Function to be in these five areas will allow you to start forming focus and goals in the later steps.

Using the Loughridge Transformations‘ Finance Functional Model in Practice

The two primary inputs for applying the Finance Functional Fit model are the strategic positioning from the first step and the enterprise process model. If no process model exists, the boundaries between the functions can be used as a starting point to whatever extent they are defined.

Taking those two inputs, you can work through each of the five blocks in the Finance Functional Fit model. Start with Protect and then work up from that foundation. From that point, you should define or refine the processes or sets of activities that fall under the CFO’s accountability.

Finance Function – Stakeholder Voices

At this point, Loughridge Transformations recommends ensuring that the Voices of the Business (VoB) and Customer (VoC) are heard. It could be via a structured interview, focus groups or a facilitated workshop. The format will vary depending on your organisation and the scale of the change you are undertaking. However, engaging appropriately with the impacted stakeholders is vital, whether a simple alteration in a business process or a complete transformation. In any event, fundamental to the eventual success of any change is understanding the VoB and the VoC. Understanding who they are, what they value, and why is vital.

Voice of the Business

The VoB may be reasonably straightforward for the Finance function and include increased profitability, revenue, long-term growth, and market share. Assuming you know your organisational strategy and have reviewed it as described in the first step, you should not be surprised by the VoB. That said, the time spent validating and confirming it is worthwhile.

Voice of the Customer

What may need to be clarified is the VoC. It can be defined as a collective insight into the needs, wants, perceptions and preferences of those individuals, teams, departments and budget holders who depend on the partnering from Finance to deliver their part in the organisation’s success. It will vary from colleague to colleague. Getting to the true VoC for your organisation will allow you to understand customer requirements. You will then be able to partner in the most impactful and effective manner. If you miss this, your change will be more challenging. The results may not answer the Voice of the Business.

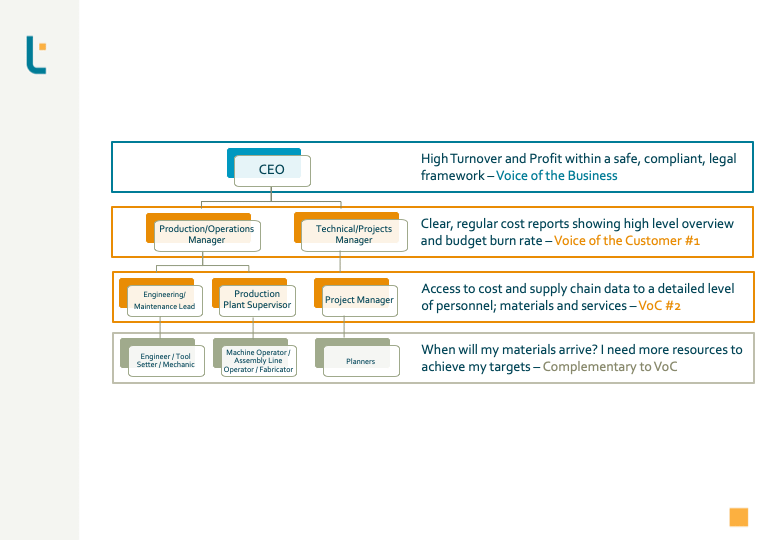

Based on our experience, the variation in Voice of the Customer in a multi-national production organisation could look something like this:

As you move down through an organisation, the needs and wants of Finance and the insight provided change considerably. Here, we could consider the CEO to be the VoB. On the other hand, Budgetholders (orange) are your true VoC, describing their expectations of Finance. Front-line operators have a valuable view. Although it is not truly part of the VoC, it provides information on perceptions of the Finance function and how the cascade through the line in your organisation works.

Scaling the Finance Functional Fit

Applying the Finance Functional Fit model in a large-scale transformation should be beginning to fall into place. What about an example at the opposite end of the spectrum? In the first step, we looked at the case of “chaotic closing”. The scenario was for an organisation in the cost-focus quadrant of Porter’s Generic Strategies. Closing is a core activity for Finance and, at the same time, often a painful or time-consuming one. Let us look at how the Loughridge Transformations Finance Functional Fit model could help.

Some Real-Life Closing Situations

Let’s imagine that your organisation operates in several geographies or there are many legal entities involved. As such, you need to produce some consolidated “group accounts”. You will want reliable and complete data sets every month and quarter, available on a timely basis. It is not unusual, in this scenario, for very few or even no one in the team to have a genuinely complete end-to-end view of all the closing activities and their dependencies. You may have experienced month- or quarter-ends with missing or inaccurate data. You might have had to re-open the books numerous times to make “last-minute” entries. Sometimes, you might even have to re-run the ERP programmes. This is especially true if you have more complex allocation cycles due to the nature of your organisation.

If you recognise any or all of these situations, the closing process may feel chaotic and sometimes inefficient. You and your team members will likely work long hours during the close. Let us look at the specifics of using the Loughridge Transformations model to improve your situation.

Applying the Finance Functional Fit Model

1: Protect

An accurate and reliable closing process is fundamental to maintaining organisational oversight. Regarding scope and strategic fit, Finance is undoubtedly on the hook for this one! Start, however, by walking through the VoB and VoC thinking. Then, engage with your stakeholders as needed.

2: Operate

Having identified closing as a core activity, in this part, we are looking at the scope and boundaries of the activities and focussing on being efficient, effective and well-controlled in what Finance does.

Define Scope

A critical factor in an efficient closing process is having a clear and agreed view of what is and is not in scope. Opinions differ on this. Some limit the close to only including the core steps in the ERP, like running depreciation or allocations. However, we have found that a more extensive interpretation of the close is ultimately more transparent and delivers higher accuracy. Practically speaking, it means including all steps directly reflected in the books and dependent steps. For example, you would include the last update of exchange rates and the actual running of the Difference in Exchange (DIE) in the ERP.

Establish Responsibilities

Establishing responsibilities and boundaries also falls in the Operate part of the model. Organisations make different choices, but having departments outside Finance involved in the closing would not be rare. It is essential to understand responsibilities and accountabilities in such cases clearly. Building on the DIE example above, an organisation may have a Master Reference Data (MRD) team or an individual responsible/accountable for entering correct exchange rates in the ERP. In contrast, the Finance (closing) team runs DIE in the close.

Identify Dependencies

Whether simple or more complicated, identifying the dependencies is also an essential piece. Let’s continue with our example of daily exchange rates. Here, it would be advisable to include a step where the MRD team confirms that they have successfully uploaded the exchange rate. DIE should only run once that confirmation is received.

3: Improve

For the closing example, when it comes to Improve, there are several potential improvements, depending on the starting point. We suggest looking at two areas in the first instance. Firstly, consider the timetable format. Various tools and forms are available, from a simple Excel spreadsheet to something like Financial Closing Cockpit (FCC), a separate module in SAP. Given the popularity of SAP as an ERP, it is worth saying a little more about it. It is a tool that gives transparency in the close (especially around accountabilities and responsibilities). It monitors how well the closing performs and highlights areas that need attention. For example, it would identify an allocation process that cannot run because the preceding step has not been completed and the close is “on hold”.

Secondly, the FCC is ideal for a centralised close, another improvement we suggest. Whether considering off-shoring or centralising in one location, the economies of scale, improved communication, and problem-solving from people sitting together are all sizeable. Because of this, co-locating facilitates a quicker and more accurate close while reducing the long hours that traditionally accompany month- and quarter-end.

FCC also enables fuller automation, which we cover in the next block.

4: Digitise

The most efficient closing processes have a 50% or higher level of automation. This reduces the need for team members to interact directly with the ERP, freeing up their time for value-adding activities while removing waiting time within the closing process. The organisation can introduce automation over time. Indeed, it is sometimes advisable to slowly increase automation as the organisation becomes more comfortable. It depends on the organisation’s requirements and the resources available.

5: Innovate

In closing, innovation is likely to be somewhat advanced, as it has been a focus of improvement over the years. Of course, we would always recommend considering the possibility of step-change or industry-disruptive ideas, but most organisations would want to exploit known improvement and digitalisation opportunities first.

What Else Should Be Considered for Finance Functional Fit?

Even though change management is not part of step two of the Loughridge Transformations method, it would be remiss not to mention it in this practical application. Having applied the model, you will likely have a close that spans a more substantial part of the organisation. As a result, dependencies and timeframes will be more critical. The close, however, is not jeopardised when one step does not occur as planned. The change management approach depends on what is changing, but ERP access is likely relevant. For example, if your organisation uses SAP, it can enable authorisation groups. The groups determine who has access to post to the ERP. This approach avoids postings in error but also helps to reinforce the rigour of the new process.

We have only scratched the surface of how you might deal with “chaotic closing” in your organisation. Changing this process is not usually a quick fix, albeit worthwhile. Depending on your current situation and the organisation’s size and complexity, a project could last six to twelve months. At Loughridge Transformations, we have years of experience working with organisations to improve their closing process. We can work with you on as many or as few elements as you need. For example, we could facilitate workshops or work with you at every stage of the way to deliver an improved process implemented successfully and sustainably.

Interested in More Finance Transformation?

Our next post will focus on the third step – defining your baseline. We will then introduce our four-component model used in assessment and design using the Loughridge Transformations method.

Have you missed some of the other posts in this series? Find them here:

-

Nine Steps to Finance Transformation

An introduction to a series of blog posts on nine scalable and modular steps to deliver successful and sustainable Finance Transformation.

-

Strategy: How to Supercharge Finance Transformation

The Loughridge Transformations approach to strategy.

-

Finance Functional Fit: The Most Critical Scope Definition You Need

The Loughridge Transformations method of determining the Finance Functional Fit – the most critical scope definition you need.

-

Baseline Definition – A Reliable Assessment Model for the Finance Function

Learn how Loughridge Transformations effectively evaluates baseline data to achieve successful Finance Transformation.

-

Define the Future – Target Setting & Benchmarking

The Loughridge Transformations structured approach to working with benchmarks and establishing targets for Finance Transformation.

-

Choose The Lever for Successful Finance Transformation

The Loughridge Transformations method of Finance Transformation: Choose The Lever – discover the tools and strategies that will set you on the path to achieving targets.

-

Finance Transformation: Understand The Context to Secure Excellence

Examining the importance of understanding what’s happening around you and identifying what could impact your Finance Transformation.

-

Power Up the Design and Ensure Robust Finance Transformation

The Loughridge Transformations approach to delivering the design phase of projects.

-

Deployment for Finance Transformation: Ensuring a Successful Go-Live

The Loughridge Transformations approach to the implementation phase of projects.

-

Sustain the Change: Finance Transformation to Last

The Loughridge Transformations way to actively reinforce the new practices and monitor their impact to pave the way to drive your Finance Transformation forward

-

Reviewing the Nine Steps to Finance Transformation

A summary of the series of blog posts on nine scalable and modular steps to deliver successful and sustainable Finance Transformation.

If you would like to speak with one of our consultants to discuss the above, please feel free to contact us!

Alternatively, take a look at our most popular blog posts:

Or are you looking for something else? Here’s what we have been blogging about recently:

Agile Analytics Associates Automation Behaviours Building Trust Business-Partnering CFO Remit Change Management Coaching Collaboration Continuous Improvement Control Design Control Framework Corporate Governance Data Deployment Digital ERP ESG Finance Function Finance Transformation Implementation Migration Off-Shoring Organisation Organisation Design Process Process Design Process Improvement Process Performance Productivity Project Management Readiness Regulatory Compliance Risk & Controls Skills sponsorship Standard Organisational Model Strategy Systems Systems Design Technology Transformation Virtual Working

10 thoughts on “Finance Functional Fit: The Most Critical Scope Definition You Need”

Comments are closed.