Define the Future – Target Setting & Benchmarking

AUTHOR: JENNIFER LOUGHRIDGE

PRINCIPAL CONSULTANT

Jennifer is a Senior Executive Finance professional with 22+ years of global experience. She specialises in Finance Transformation, ESG and Continuous Improvement, with particular expertise in Strategy, Performance Management, Business Partnering, Commercial Decision-Making, Corporate Governance and Valuation.

In our last post in this nine-part series, we examined Baseline Definition: a Reliable Model for Assessing the Finance Function. We covered the four-component sequence used in assessment and, later, design.

This post will focus on the fourth of the nine steps: Define the Future—Target Setting & Benchmarking. Here, we will examine realistic target setting and understanding “what good looks like.”

Target Setting

If you have followed the Loughridge Transformations method, you will already have looked at strategy and functional fit and assessed the baseline. With these steps complete, it is time to define aspirations and target setting.

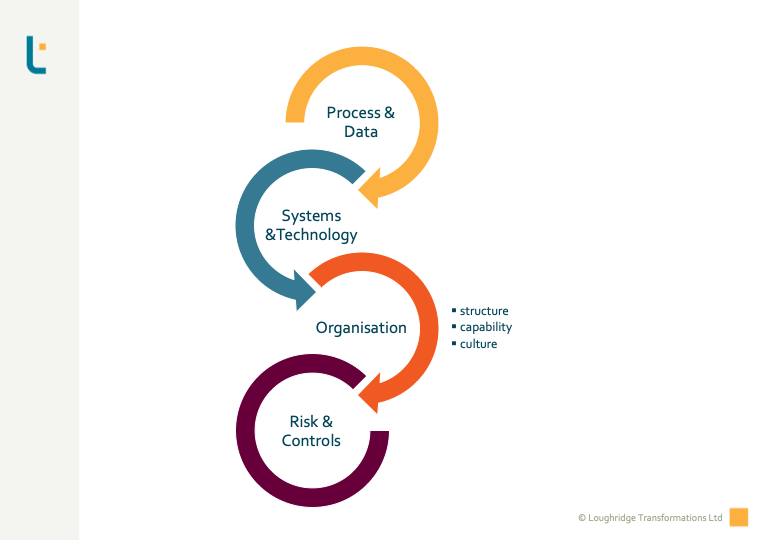

Using the strategy and functional fit, you can start to define at a more granular level where you would like the finance function to be. At Loughridge Transformations, we find using our four-component model introduced in the last post helpful.

Target Setting: Strategic Objectives

You should set strategic objectives for each component in the model. At Loughridge Transformations, we like visualising this as a road with boulders and small stones.

Using the baseline assessment we covered in the last post as a starting point or the beginning of the road, you determine where you want to be in the future or at the end of the road.

Then, think about the giant boulders that will need to be removed as you go along the road. These are the three- to five-year objectives. For example, you can use the Hoshin Kanri approach for each boulder. In our last post, we referred to Hoshin Kanri, another element of the Kaizen philosophy. It can be explained as an approach that steers you from strategic to tactical.

Lastly, come the small stones. We rely on individual work teams’ insight and ingenuity to remove these stones from the road. To do that, teams can use a continuous improvement mindset to identify and implement improvements within their sphere of influence.

Fair enough, you might say, but how do you know what the end of the road should be in the first place? Inevitably, you will need some judgment to set suitable targets for your organisation. It rather depends on the nature of your organisation and the culture around targets, in general. There are, however, some things you can consider as you try to identify what those targets should be.

Voice of the Business: What Do They Need? What Do They Want?

In our post on Finance Functional Fit, we discussed the Voice of the Business and the Voice of the Customer. Now is a great moment to revisit and, if necessary, deepen what you did there. It may be that your organisation is, for example, looking for improvement. However, even if the VoB or VoC only indicates a need for cost savings, there will likely be a requirement for business continuity on critical processes or processes that touch certain parts of the organisation. Now, reflect, firstly, on the “needs versus wants”. Secondly, on that for which the end customer or shareholder is willing to “pay”.

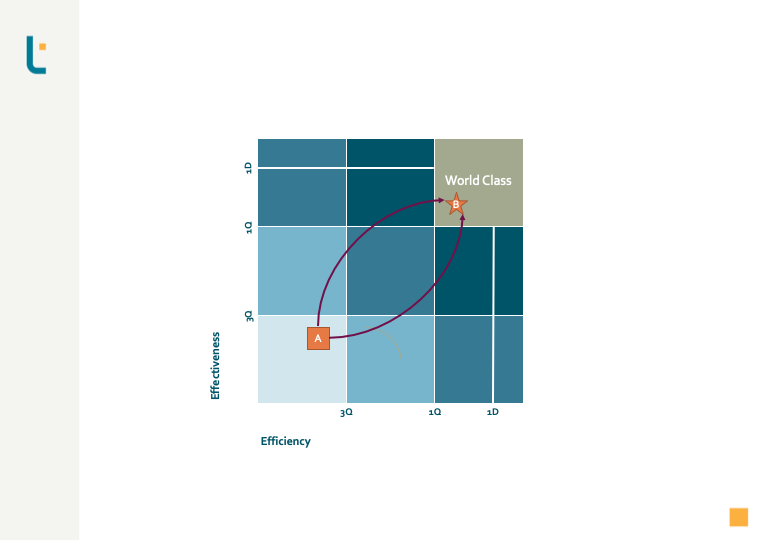

What Does Good Look Like?

Benchmarking can be a valuable data point. However, it depends on the scale of transformation that you are undertaking. Internal or external benchmarking and leis or more formal benchmarking may be appropriate. Data is available per process for top-quartile and world-class performance, usually looking at efficiency and effectiveness.

This data is, of course, not static. The goalposts shift as organisations take steps to transform how they operate. Process measurement can be at different levels of sophistication. Benchmarking can range from bringing in benchmarking specialists, involving consultants like Loughridge Transformations with relevant know-how, to reading and researching the topic.

Target Setting: Keeping It Real

After all that, you need to set realistic and achievable targets, albeit stretching. Your baseline from the previous step will give your starting point. If the gap versus your aspiration is large, phasing targets and, ultimately, the delivery can often make sense.

Target Setting & Benchmarks – A Practical Example

Off-Shoring Fixed Assets Accounting

Let’s look at a practical example of how the Loughridge Transformations method would apply. Suppose that, in principle, off-shoring this process fits with the organisational strategy and finance functional fit. We will also assume that the baseline assessments are complete. Our focus is on target setting and benchmarks, so we will not look at that here. That also means we will not discuss off-shoring holistically or evaluate Shared Service Centres versus Outsourcing.

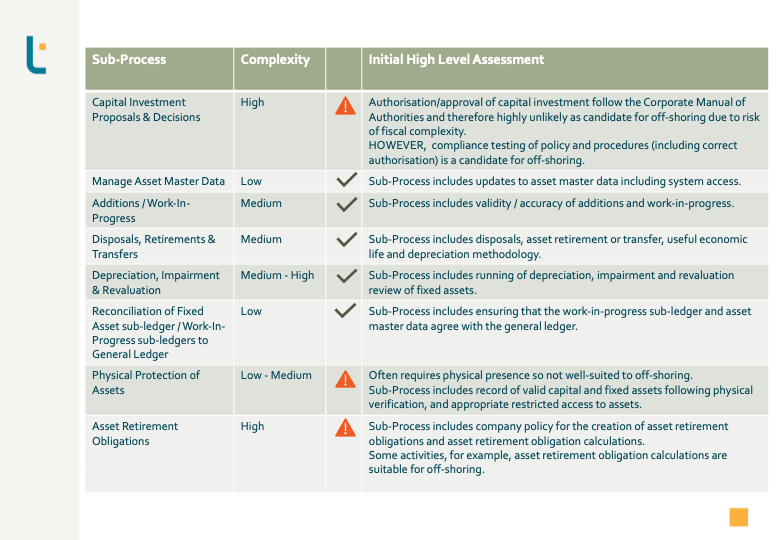

The Fixed Assets Accounting process covers various activities, including capital investment proposals, impairment testing, and pure transactional processing. You quickly arrive at the target setting and benchmarks question when considering off-shoring. You have to identify which activities are suitable for off-shoring and the impact of any process re-design on the end-to-end process. Some things to consider at this point are:

- Which activities can we off-shore?

- VoB: only finance-to-finance; only Finance; Finance and non-finance – whatever gives the best process performance?

- Only low complexity?

- What represents good, better and best?

- Will we need to re-design the process?

- What is the tolerance of process performance during and after off-shoring?

- Should we take a phased approach or go for a “big bang”?

Building the Roadmap

You can use suitable project and change management tools to increase your chances of success. However, we will not go into detail on that here. That is the subject of a later post in the series.

Whatever tools you choose, we strongly recommend that you work on the project in a very structured manner. Making significant changes in the operation of critical processes requires careful consideration and risk mitigation. Many steps along the way must be done “first-time-right.” There will often not be a second chance, and the remediation effort can be painful, time-consuming and costly.

If your organisation is taking on this for the first time, it is worth bringing in experience and expertise. Applying practical experience can be one of the most significant mitigating actions. In the long run, it can save you substantial costs. Furthermore, it helps you avoid reputation issues.

The Key Steps or Boulders on the Roadmap

1. Mapping the End-To-End Process

Regardless of the process earmarked for off-shoring, we recommend an initial assessment and breakdown into sub-processes. You can obtain an end-to-end overview of the process and give an early warning sign of potential challenges and risks.

It is also helpful to make an initial assessment of each sub-process, looking at its suitability for off-shoring and complexity. Views on this can, of course, differ from person to person. However, as a rule of thumb, the net should be cast as wide as possible. At this point, only legal or very obvious practical hurdles should be considered to prevent the off-shoring of a sub-process.

Here, we have broken down the Fixed Assets Accounting process into sub-processes:

Now, you have a high-level view of the potential scope for off-shoring.

Your next step should be to break the sub-processes down further into activities.

2. Mapping Activities

In this step, you should include the department and the role or job responsible for performing the task to get a view of the people potentially impacted. Although the change management, employee engagement and consultation aspects are significant, we will not go into details here—these would need to be included in the Hoshin Kanri and eventual project plan.

As this is for illustrative purposes only, we have chosen just one sub-process for this step. Of course, you must go through the same exercise for all sub-processes.

At this point in your off-shoring project, you will have identified the activities with potential for off-shoring and the departments, roles, and perhaps individuals executing them.

Next is activity execution analysis. This analysis includes where and when the activities are performed.

3. Activity Analysis

At this stage, you should be able to perform due diligence or activity analysis. The analysis should cover how and where the activity is executed and any associated financial controls.

Again, for illustration, we have only chosen a couple of activities:

You should now have enough to start drafting a migration plan. Please note that our illustrations are meant to serve as a partial list of tasks you must complete. They are intended to give a high-level flavour of what is involved in off-shoring.

Target Setting: What Else to Consider?

We have examined the scoping and advocated not limiting activities that could be in scope too early. However, when setting targets, you should consider several other aspects.

End-to-End Process Migration

A common pitfall is thinking that you mitigate the risks by only migrating part of an activity. Unfortunately, the opposite is often the case. For example, you migrate running depreciation while maintaining the review and approval on-shore. The (unintended) consequence is that you dilute accountability and incur additional costs and inefficiencies. As a rule, you should always migrate end-to-end activities in the process. This approach eliminates the ambiguity in accountabilities.

The actual risk mitigation is to phase the migration of more complex processes. This approach ensures that the controls and control owners are updated to match the potentially different risks in executing any particular process step.

Maintaining Process Performance During Migration

If you have followed the Loughridge Transformations method, you will already have baseline process performance. It is an essential step. You must get precise data on how well the process or activity performs on-shore. If your organisation does not routinely measure process performance, this can, in itself, be eye-opening.

Either way, you must monitor performance during and after migration to ensure that it meets your established criteria in the VoB or VoC. This monitoring could feed into Service Level Agreements or Process Key Performance Indicators. In addition, a performance review should form part of the on- and off-shore ways of working.

Knowledge Retention

Almost all organisations committed to offshoring will have faced the challenge of losing process knowledge and expertise. In the worst examples we have seen, process performance can deteriorate dramatically, sometimes even causing processes to fail to operate altogether. Again, attempts to mitigate this risk often involve retaining staff in the on-shore location to check and assist the off-shore process operator when processes break down.

To properly mitigate this risk, you must migrate process knowledge to process experts in line with the process steps. Of course, ways of working also need to reflect this, and process-expert roles should be defined separately from process-operator roles. But, again, standardising the process makes this vastly more feasible and cost-effective.

Ship and Fix or Fix and Ship?

We just mentioned the role of standardisation in managing knowledge retention. Standardisation will incur an additional upfront cost, but the overall business case is typically robust. Process re-design can be necessary for more complex processes. Where possible, we recommend doing this before migration. It may delay the migration, but the cost and time involved in training the shared service or outsourced team members in outdated, broken, inefficient or localised processes can be significant.

There can be scenarios where the cost-benefit ratio works differently than above. It depends on the on-shore organisation’s culture, skills, and capacity. For example, standardisation efforts may have previously been unsuccessful and resistance to change may be high. So, even though it is a more expensive approach—mitigating those additional risks can be costly—it may still be the better approach to standardising and otherwise improving process performance after migration.

A Phased Approach or “Big Bang”

The choice mainly depends on the maturity of your existing shared services or outsourcing partner. However, it is advisable to start with the lowest complexity activities and gradually increase migration penetration as a rule of thumb. Remember to consider process and data, systems, organisation, and controls. After all, to give a small example, a control half-executed in one team and half-executed in the other is unlikely to be the best set-up.

Exercising Judgement…

Undoubtedly, this fourth step in the Loughridge Transformations method of Finance Transformation requires considerable judgement. Understanding your organisation’s culture and appetite for improvement is critical. Luckily, Finance often has excellent insight into what works or does not work well in the organisation’s annual and longer-term planning and target setting, indicating the organisation’s culture in this arena. Next, properly appreciating the risks and the mitigating actions will keep the targets realistic and achievable.

Interested in More Finance Transformation?

Our next post will focus on the fifth step, choosing the lever. This involves determining how to reach targets and creating the foundation for solution selection in the design phase.

Did you miss some of the other posts in this series? Find them here:

-

Nine Steps to Finance Transformation

An introduction to a series of blog posts on nine scalable and modular steps to deliver successful and sustainable Finance Transformation.

-

Strategy: How to Supercharge Finance Transformation

The Loughridge Transformations approach to strategy.

-

Finance Functional Fit: The Most Critical Scope Definition You Need

The Loughridge Transformations method of determining the Finance Functional Fit – the most critical scope definition you need.

-

Baseline Definition – A Reliable Assessment Model for the Finance Function

Learn how Loughridge Transformations effectively evaluates baseline data to achieve successful Finance Transformation.

-

Define the Future – Target Setting & Benchmarking

The Loughridge Transformations structured approach to working with benchmarks and establishing targets for Finance Transformation.

-

Choose The Lever for Successful Finance Transformation

The Loughridge Transformations method of Finance Transformation: Choose The Lever – discover the tools and strategies that will set you on the path to achieving targets.

-

Finance Transformation: Understand The Context to Secure Excellence

Examining the importance of understanding what’s happening around you and identifying what could impact your Finance Transformation.

-

Power Up the Design and Ensure Robust Finance Transformation

The Loughridge Transformations approach to delivering the design phase of projects.

-

Deployment for Finance Transformation: Ensuring a Successful Go-Live

The Loughridge Transformations approach to the implementation phase of projects.

-

Sustain the Change: Finance Transformation to Last

The Loughridge Transformations way to actively reinforce the new practices and monitor their impact to pave the way to drive your Finance Transformation forward

-

Reviewing the Nine Steps to Finance Transformation

A summary of the series of blog posts on nine scalable and modular steps to deliver successful and sustainable Finance Transformation.

If you would like to speak with one of our consultants to discuss the above, please feel free to contact us!

Alternatively, take a look at our most popular blog posts:

Or are you looking for something else? Here’s what we have been blogging about recently:

Agile Analytics Associates Automation Behaviours Building Trust Business-Partnering CFO Remit Change Management Coaching Collaboration Continuous Improvement Control Design Control Framework Corporate Governance Data Deployment Digital ERP ESG Finance Function Finance Transformation Implementation Migration Off-Shoring Organisation Organisation Design Process Process Design Process Improvement Process Performance Productivity Project Management Readiness Regulatory Compliance Risk & Controls Skills sponsorship Standard Organisational Model Strategy Systems Systems Design Technology Transformation Virtual Working