Baseline Definition – A Reliable Assessment Model for the Finance Function

AUTHOR: JENNIFER LOUGHRIDGE

PRINCIPAL CONSULTANT

Jennifer is a Senior Executive Finance professional with 22+ years of global experience. She specialises in Finance Transformation, ESG and Continuous Improvement, with particular expertise in Strategy, Performance Management, Business Partnering, Commercial Decision-Making, Corporate Governance and Valuation.

In the second step in this nine-part series, we looked at the Finance Functional Fit. First, we looked at using the organisation’s strategic positioning. We then applied a Loughridge Transformations model to determine the strategic fit of the Finance Function, which you might also call the CFO Remit.

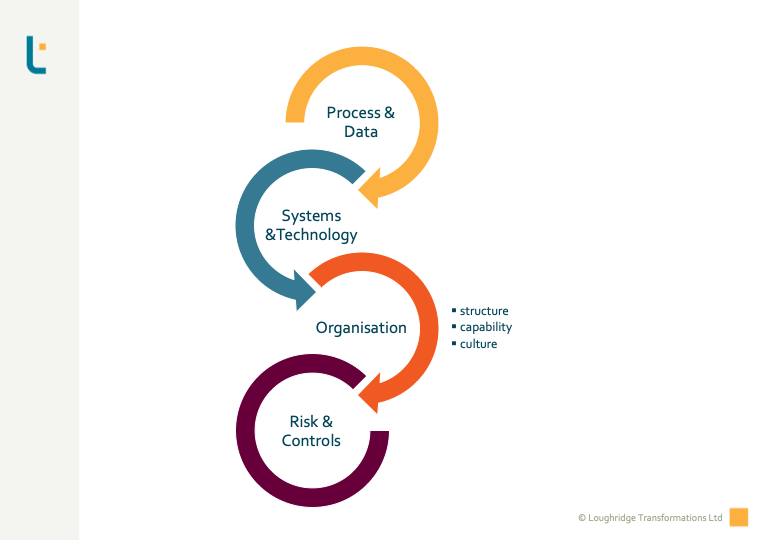

Having defined the scope, we must review the Finance Function’s current state. To do this review, we use the Loughridge Transformations four-element sequence for the baseline assessment. The sequencing is not too consequential for this step but will become critical later in the design stage. However, it always helps to start as you mean to go on, so we recommend using this sequence during the assessment- i.e. now.

Defining the baseline consists of assessing where the organisation is today. The approach is scalable, as with other parts of the Loughridge Transformations method. For example, you might be dealing with a complete process map for the Finance Function. On the other hand, zoom in on one particular process or set of activities. Either way, the method is the same.

Using the Four-Element Model in Baseline Assessment

It is possible to perform baseline assessments on a very detailed level. For example, you can use third parties who specialise in benchmarking. However, using experienced consultants like Loughridge Transformations can be more cost-effective. On the other hand, you might want to gather critical team members in self-assessment workshops. Whatever scale you are operating at and however you choose to go about it, the four components you should assess are:

We’ll cover the sequence’s specific rationale when discussing the detailed design. However, the initial purpose is to ensure you catch everything during the assessment.

Let us look at each of the four parts of the sequence:

Baseline Assessment: Process & Data

Gartner has set the standard for assessing the maturity of processes and data within organisations. Even though they created their original process model over ten years ago, it remains valid. Their data model, however, is a more recent development, works on the same principle, and is equally well-regarded. At one end of the scale, you can bring them in to do a complete assessment on your behalf. It is also possible to buy access to their documentation and use it to perform self-assessments.

If you are working on a much smaller scale, you can, however, facilitate an internal assessment based on organisational knowledge and analysis. But, again, it depends on the complexity and size of your organisation and its ultimate aims. Whichever way you choose, the goal is to ascertain the maturity level for both process and data within your organisation.

Baseline Assessment: Systems & Technology

The assessment’s primary aim is to determine the level and effectiveness of manual versus automated process steps within the processes in scope. Depending on your organisation’s circumstances, that will vary hugely from under-utilising the current technology, such as the ERP, to technology no longer fit for purpose. Indeed, most organisations need to continuously better exploit technology in a world with increasing digital opportunities. Developments in this arena come thick and fast, and solutions are superseded quickly.

The challenge here is often knowing where to start and which indicators to review. Using external expertise and, notably, experience in process, data and systems, such as the consultants at Loughridge Transformations, can be altogether worthwhile. We illustrated this in the second step with the financial closing process – chosen for its labour intensity. In that example, the volume and nature of the manual journal entries spotlight whether the system or systems are fully utilised, under-utilised, or no longer fit for purpose. With experience, you or one of our consultants can interrogate these and other data points to understand the “as-is” situation.

Baseline Assessment: Organisation

At Loughridge Transformations, we think about organisation in three parts: Structure, Capability and Culture. Looking at any documentation and “Going to Gemba” is critical at this point. Gemba is part of the Kaizen philosophy, where processes, for example, are observed to understand what occurs in reality instead of what exists on paper. If you are unfamiliar with the approach, why not arrange a call to find out how we introduce and coach the technique – amongst others from the Kaizen philosophy – with leaders in your organisation?

Structure

Assessments here include reviewing formal or informal organisation charts and job or role descriptions if they exist. The review also covers locations where the activities are physically performed. Often, documentation is more of a snapshot than something routinely updated. As a result, going to Gemba can be a tremendously insightful part of the assessment.

Capability

Next, we recommend evaluating the organisation’s skills and (collective and individual) competency level. This assessment is not absolute but relative to the roles or jobs identified when looking at Structure. While making the assessment, looking for over-capacity and under-capacity is vital.

This assessment can be sensitive for people in the organisation. So, it is essential to consider how these assessments are done, especially if you intend to use them in a later selection process. We highly value how team members experience these and other reviews at Loughridge Transformations. It should be fair, respectful, transparent and robust.

Culture

Last, we suggest examining current behaviours and team dynamics. This helps make intelligent change management decisions. Even more importantly, it is where you gather insight into how people operate alone and with others. Whether you want to sustain or change this within your organisation, you must first understand it. Given how critical people are within any Finance Function, you risk overlooking a valuable transformation differentiator—and not giving people the respect they deserve during transformation!

Baseline Assessment: Risk & Controls

At this time, you have now reviewed the status of the processes in scope. You have also analysed the degree of automation and the organisational elements. The final part of the sequence examines the (internal) risk and control framework. Whatever the scale of the organisation, the internal controls are there to protect the assets and ensure regulatory and fiscal compliance. For this reason, you want data quality that can be assured and evidence-based. As a result, a robust control framework will include preventative systems controls, detective IT-dependent controls and detective manual controls.

A typical assessment will look at the risks within the process. It will consider the degree of automation, who does what, and where they do it. It includes validation that the controls are addressing the risks. Excess controls can result in a “tick-box” exercise for the control operators. The control points are often more akin to a process step description than demonstrable mitigation of the process risk – design ineffective. Too few controls can mean risks are overlooked and mitigation is lacking. Alternatively, sometimes the net is cast so widely that the control lacks clarity on the risk or risks supposedly being addressed.

Using Loughridge Transformations‘ Method on a Smaller Scale?

By now, how to apply the assessments within a large-scale programme may be more apparent. We advocate this method at Loughridge Transformations, regardless of the scale. Let us illustrate why with a practical example.

Baseline Assessment: A Practical Example – Joint-Venture Billing

You work in the oil and gas sector. Your department is responsible for the audits prescribed in the joint-venture agreements forming the commercial structure for operating the fields. Your small team is overwhelmed by the number of audit findings and the time needed to resolve them. There have been instances where these audit findings have led to legal disputes. You agreed with your manager to address this exposure for the organisation. There may also be under-billing to the joint-venture partners. Although the joint-venture partner auditors will highlight over-billing, they are less likely to seek under-billing.

You already know that boosting your team with temporary resources may address the backlog in the short term but will not fix the underlying causes. Assessing the current status using the four-element sequence should allow you to understand the issue and give you the correct input to make successful and sustainable changes.

Your team is overwhelmed with today’s issues and trying to prevent them from worsening. Therefore, bringing in some consultants, such as Loughridge Transformations, to facilitate the baseline assessment could prove worthwhile.

Process & Data

In our example, the joint-venture agreements form the basis of both process and data. The process is sometimes explicitly detailed or might be only implicit. Either way, the first step in the assessment determines whether the actual real-life process matches the agreement. Next, you must validate if the Master Reference Data (MRD) is in line. As things do not remain constant, the process and data assessment should also include the process steps for updates and the appropriate frequency of validation checks (for example, before month- or quarter-end) for new cost centres or profit centres.

Systems & Technology

This assessment looks at which process steps are manual, spreadsheet-enabled or ERP-enabled and where the potential for increased automation would lead to time savings or higher accuracy. Ascertaining which ERP reports are available (and in use) to highlight gaps or other MRD errors and understanding whether billing statements are auto-generated would be part of this assessment. As mentioned above, looking at Manual Journal Entries is always a giveaway in process performance and automation. In our experience, these assessments often show improvement opportunities, especially if only some organisation members have detailed systems knowledge. That frequently arises when key individuals have moved on or retired since the installation of core technology.

Organisation

A process like joint-venture billing will likely involve several departments. This likelihood increases if the organisation has offshored or outsourced specific process steps. Almost certainly, not all of these departments will be within Finance. Assessing who does what and when they do it is vital in understanding opportunities for improvement. You should review the skill and capability levels and team dynamics. Does each process operator have the appropriate knowledge, equipment and ability to perform their step in the process? What is the degree of communication and teamwork across the process? What is helping or hindering the team’s effectiveness?

Risk & Controls

Lastly, with the above information, you can look at the control framework as it applies to this process. Already, there is an indication of control problems – for instance, the number of findings and your feeling of under-billing. First, you have to understand the reality of the process compared to the agreements. Then, you have to review which steps are manual or otherwise. Last, you must investigate who is doing what, whether they are appropriately skilled, and how well they work together. With this, you can assess the risks and determine whether the existing controls are mitigating the “right” risks in the “right” way.

The Road to Resolution?

Using the Loughridge Transformations method, you know you have a complete enough understanding of your current situation. In all likelihood, working through the baseline assessment will have highlighted some improvement opportunities already. Your team could implement some of those opportunities in the short term. You could make easy gains and create breathing space to tackle the remainder. The rest of the insight gained feeds into subsequent transformation steps. By approaching your challenges in a structured manner, you have the highest chance of success and sustainability. It also makes it much more manageable for busy teams.

Interested in More Finance Transformation?

Our next post in the series focuses on the fourth step – define your future. We will look at setting targets and using benchmarking to inform your aspirations.

Did you miss some of the other posts in this series? Find them here:

-

Nine Steps to Finance Transformation

An introduction to a series of blog posts on nine scalable and modular steps to deliver successful and sustainable Finance Transformation.

-

Strategy: How to Supercharge Finance Transformation

The Loughridge Transformations approach to strategy.

-

Finance Functional Fit: The Most Critical Scope Definition You Need

The Loughridge Transformations method of determining the Finance Functional Fit – the most critical scope definition you need.

-

Baseline Definition – A Reliable Assessment Model for the Finance Function

Learn how Loughridge Transformations effectively evaluates baseline data to achieve successful Finance Transformation.

-

Define the Future – Target Setting & Benchmarking

The Loughridge Transformations structured approach to working with benchmarks and establishing targets for Finance Transformation.

-

Choose The Lever for Successful Finance Transformation

The Loughridge Transformations method of Finance Transformation: Choose The Lever – discover the tools and strategies that will set you on the path to achieving targets.

-

Finance Transformation: Understand The Context to Secure Excellence

Examining the importance of understanding what’s happening around you and identifying what could impact your Finance Transformation.

-

Power Up the Design and Ensure Robust Finance Transformation

The Loughridge Transformations approach to delivering the design phase of projects.

-

Deployment for Finance Transformation: Ensuring a Successful Go-Live

The Loughridge Transformations approach to the implementation phase of projects.

-

Sustain the Change: Finance Transformation to Last

The Loughridge Transformations way to actively reinforce the new practices and monitor their impact to pave the way to drive your Finance Transformation forward

-

Reviewing the Nine Steps to Finance Transformation

A summary of the series of blog posts on nine scalable and modular steps to deliver successful and sustainable Finance Transformation.

If you would like to speak with one of our consultants to discuss the above, please feel free to contact us!

Alternatively, take a look at our most popular blog posts:

Or are you looking for something else? Here’s what we have been blogging about recently:

Agile Analytics Associates Automation Behaviours Building Trust Business-Partnering CFO Remit Change Management Coaching Collaboration Continuous Improvement Control Design Corporate Governance Data Deployment Digital ERP ESG Finance Function Finance Transformation Implementation Migration Off-Shoring Organisation Organisation Design Process Process Design Process Governance Process Improvement Process Performance Productivity Project Management Readiness Risk & Controls Skills Solution Selection sponsorship Standard Organisational Model Strategy Systems Systems Design Technology Transformation Virtual Working